Do you know the differences between revenue, income, profits, and cash flow? Although the terms may be used interchangeably in casual conversation, they do have distinct meanings. Understanding what these terms mean will help you appreciate how each of them affects your business. This article explains the differences between them.

1 Revenue

Revenue, at its most basic, is the amount you earn from customers from sales of your product or service, before considering the costs of your product or service or the costs of any operating expenses. It is often referred to as the “top line,” as it is the first line item on your income statement or statement of operations.

Revenue does not include amounts raised from investors or amounts borrowed from lenders. These items are classified as equity and debt, respectively, and do not directly affect the income statement.

Revenue also does not include interest income (unless you are in the business of lending money) or the amounts received from the sale of items to others that are not part of your ordinary operations and activities, such as the proceeds from excess or obsolete equipment. These items are usually classified farther down in the income statement as other income, as they are often usually only a small part of the company’s total operations.

You may sometimes hear about gross revenues and net revenues. Generally, a company’s business model will determine whether it can recognize revenue on a gross or net basis.

1.1 Gross Revenue

If a company acts as a principal in a transaction, meaning that it controls the goods or service before it is transferred to the customer, then it recognizes revenue on a gross basis, meaning the total amount earned from the customer on the sale.

An example of a principal is a manufacturer of retail goods who sells goods directly to end customers.

1.2 Net Revenue

However, some companies act as agents in transactions, meaning that they help facilitate the transaction but do not control the underlying goods or services before they are transferred to the customer. Rather, they earn a commission or fee for each successful transaction completed. In these cases, agents must recognize revenue on a net basis, meaning that only their commission or fee is recognized as revenue.

An example of an agent is someone who helps arrange a transaction between the provider and the end customer, like a travel agent arranging flights—it’s pretty clear that it is the airline providing the air service and not the travel agent. Other less clear examples of agents include affiliate marketers who earn referral fees and companies that store and sell products on behalf of the seller without taking ownership of them (often known as consignment).

2 Income, Profits, and Margins

Income and profits can be used more interchangeably with one another. At their simplest, income and profits represent what you have left over after expenses have been deducted from revenues.

On the financial statements, income is often broken out into two figures: gross profit and net income.

2.1 Gross Profit

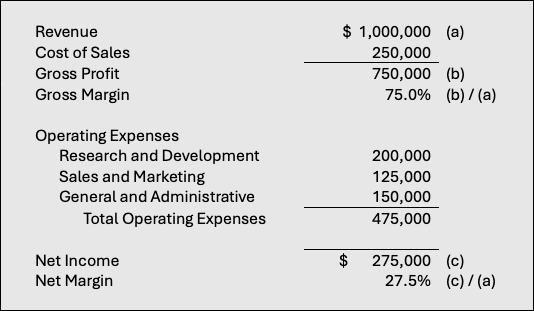

Gross profit is your revenue less the costs directly associated with the product or service. These can include things such as the costs of materials, labor, and facilities and equipment that are directly associated with the production and delivery of the product or service, which are often collectively referred to as the costs of sales or costs of goods sold.

2.2 Net Income

Net income takes gross profit and deducts other expenses that are not part of the costs of sales or costs of goods sold. These include research and development, sales and marketing, administrative expenses, taxes, and interest expense and income. Collectively, these often comprise a significant amount of the operating costs of a company.

2.3 Margins

Margins are simply the profits or income divided by your revenue, expressed as a percentage. Gross margin is the percentage obtained by dividing your gross profit by revenue. Similarly, net margin is the percentage obtained by dividing your net income by revenue.

Margin percentages are often quoted and analyzed because they standardize comparisons across companies and reflect how much you make from your product or service.

The following table illustrates how revenue, gross profit, and net income are shown on an income statement or statement of operations.

3 Cash Flow

Cash flow is a measure of how much cash has been generated or used over a period of time. Here’s where things get tricky: cash flow is not the same as net income, because net income is determined based on accounting rules for revenues and expenses that may not correspond to the actual movements of cash. This is because accounting attempts to match revenues and expenses to the periods over which they are earned or incurred.

For example, you may receive a large upfront cash payment from a customer for a contract to be fulfilled over the next year, but the revenue may need to be recognized over that time period (more below in the section on revenue recognition). Similarly, you may make a large cash purchase for a major piece of equipment that will last you for five years, but the cost of that outlay is not recognized all at once on the financial statements, but rather as depreciation expense taken over the life of that equipment.

Cash flow is the most important measure to an early-stage startup, since it will dictate how long the startup can operate before it runs out of cash, and how quickly the startup will need to raise new capital or financing. The cash usage is typically referred to as the burn rate, and often expressed in terms of how many months of cash the startup has left at that burn rate.

As a startup begins selling product, generating revenue, and scaling, the focus shifts from cash burn to growing revenue and achieving positive margins.

3.1 The Statement of Cash Flows

So how do you determine cash flow if it is not equal to the accounting net income? Well, there happens to be a financial statement called the statement of cash flows that does exactly that—it reconciles the income statement to cash flows. The statement of cash flows helps answer specific questions that aren’t revealed by the income statement, such as:

- Where did the company obtain its funds from?

- What use was made of net income?

- How does net income compare to cash flows?

- How much capital was generated internally as opposed to from external sources?

- Is the business expanding faster than it can generate funds?

The statement of cash flows breaks down cash flows into three areas: operating, investing, and financing activities. Operating activities are those related to the day-to-day operations and expenses of the company. Investing activities are less frequent, but relate to those activities that generally have a longer-term impact on the company, such as buying factories and equipment. Financing activities consist of those related to raising and repaying capital and debt.

Of the three types of cash flows outline above, operating cash flow is the most relevant and similar to cash burn as it encompasses most of the cash flows. However, a company should not ignore planned and required investments and financing activities when it prepares its cash burn forecast.

4 How Revenue Recognition Affects Revenue and Cash Flows

As alluded to earlier in this article, there are well-defined accounting rules that determine when revenue can be recognized in the income statement, independent of cash flows. This is because of the concept that revenue is earned by a seller only as certain requirements with a customer are satisfied. The revenue recognition rules are specified in Accounting Standards Codification 606 (also known as ASC 606), Revenue from Contracts with Customers. A full description of ASC 606 is beyond the scope of this article, so we will only focus on some basics here.

To see how revenue recognition differs from cash flows, let’s consider the following examples:

4.1 Example 1: Sale of a Physical Product

Take a simple transaction where the company sells a piece of hardware to a customer for $100,000. They customer is required to make a deposit of $20,000 today, with the remaining balance of $80,000 to be paid one month after the company ships the hardware. The company has no further obligations to the customer after the hardware is shipped. Let’s look at each piece of this transaction:

- Company receives customer deposit of $20,000 – The company cannot recognize the $20,000 received as revenue as they still have to deliver the hardware. However, the $20,000 does count as cash received, so it does result in positive cash flow. Instead of being recognized as revenue in the income statement, the $20,000 is instead recorded as deferred revenue, a liability on the balance sheet, for the time being.

- Company ships the hardware – At this stage, no cash is exchanged. However, the company has satisfied its obligation to the customer, and so it can recognize the value of the contract of $100,000 as revenue. The company will send an invoice to the customer for the remaining balance of $80,000, which will appear as a receivable on the balance sheet. At the same time, the deferred revenue of $20,000 from the first step is transferred to revenue.

- Company receives the $80,000 payment – When this happens, the receivable of $80,000 is relieved, and there is positive cash flow of $80,000. No additional revenue is recognized as it was all recognized in the previous step when the hardware was shipped.

The above is a simple example for a sale of a physical item with no further obligations to the customer. In reality, there are often other items in a contract such as support or consulting services, or software may be sold on a subscription basis for an upfront annual payment. These kinds of situations accentuate the differences between revenue and cash flow, which are illustrated in the next example.

4.2 Example 2: SaaS Subscription Revenue

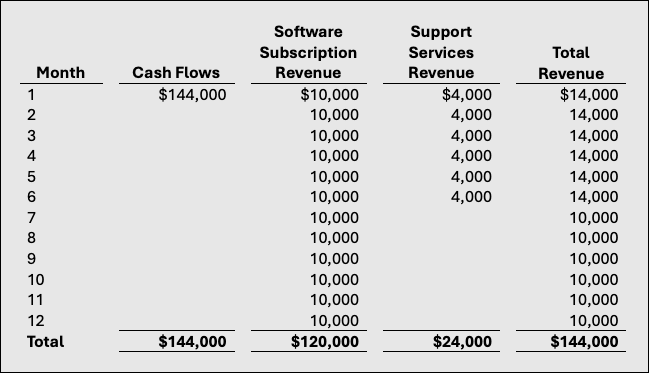

Now let’s look at an example for a software-as-a-service transaction. In this example, suppose the contract is for a cloud-based SaaS subscription for a term of 12 months, and the company also provides support services for the first 6 months. The total contract is for $144,000, payable up front. Here’s how the revenue and cash flows break down:

- At signing of the contract – Assuming the contract is effective at the time of signing and the customer pays immediately, then $144,000 of cash will be received immediately, resulting in positive cash flow at the very beginning of the contract. However, revenues must be apportioned between the software subscription and the support services. Suppose the software subscription is worth $120,000 and the support services are worth $24,000.

- Software subscription – Since the $120,000 software subscription is for a term of 12 months, only $10,000 of revenue can be recognized each month. The reason for this is because even though the company has provided access to the software to the customer, it has an obligation to provide this over time.

- Support services – Since the $24,000 of support services are provided over a term of 6 months, $4,000 of revenue can be recognized each month for the first six months.

The table below shows how the revenues can cash flows are treated for the above contract:

The result of this contract is that even though cash flows are received upfront, the revenues that are recognized on the contract are spread out over time. Furthermore, since the support services only last for 6 months, revenues are lower in the second half of the contract.

5 Final Words

Understanding the distinctions between revenue, income, profits, margins, and cash flow is crucial for businesses of all sizes. Revenue represents the total income from sales, while income and profits reflect the remaining amount after deducting expenses. Margins measure the profitability of operations, and cash flow indicates the actual movement of money into and out of the business. Finally, revenue recognition and accounting rules create differences between reported profits for accounting purposes and actual cash flows.

By effectively understanding the differences in these financial metrics, you and your startup can communicate effectively with investors and make informed decisions to achieve long-term success.